Establishment & PF Audit

In the audit of establishment charges, rules contained in Indian Railways Establishment Code, Chapter VIII of Indian Railway Financial Code, Vol. I, Chapters VIII, X and XII of Indian Railway Administration and Finance, Chapter XVI of Indian Railway Establishment Manual, Vol. I, Chapter VIII, XII and XIV of Indian Railway Accounts Code Vol. I., any special rules and procedure approved by competent authorities for individual Railways as well as the instructions contained in Chapter 2-6 of MSO (Audit) are adhere to.

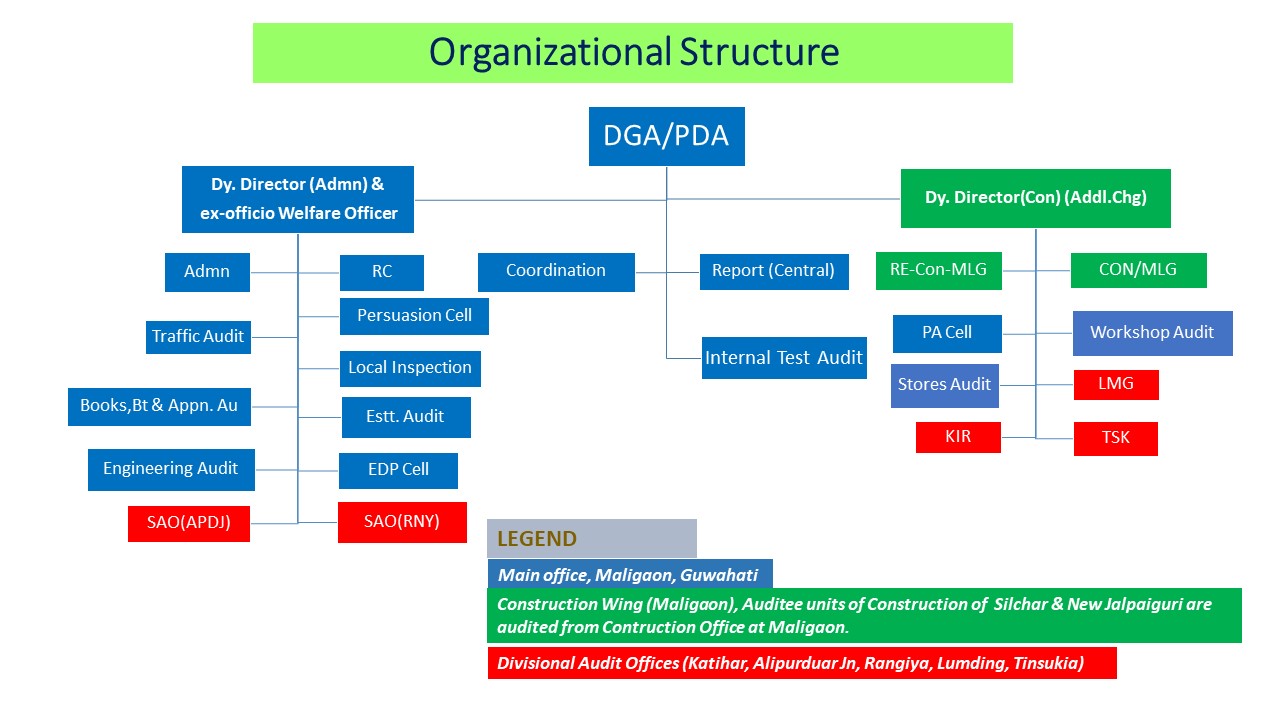

The audit of Establishment matters consist of the following:

Auditee Units:-

Personnel office of Zonal Headquarters as well as Construction Organisation at Headquarter, Divisional Personnel offices at Katihar, Alipurduar, Lumding, Rangiya, Tinsukia and Workshop and Stores Personnel offices at Dibrugarh and New Bongaigaon.

- Audit of Sanctions relating to Establishment matters

- Computerised Pay roll system

- PF Accounting

- Audit of Pay Bills

- Increment, Revision of Pay, Allocation

- Audit of Officiating Appointment

- Arrears of Pay

- Payment of cash equivalent of leave salary

- Advance of Pay, Travelling Allowance, Purchase of Conveyances

- Rent of Residential Buildings

- Audit of Passes & PTOs

- Contingent Vouchers

- Leave Account, Fixation

- Medical Attendance Bills

- Audit of Provident Fund, Temporary Withdrawals, Final Withdrawals

- Audit of Accounts of Staff Benefit Fund

- Railway Employees Insurance Schemes

- Productivity Linked Bonus

- Reconciliation with General Books etc.