Direct Tax Audit of Shell companies

By Mr. Alwyn Furtado, Senior Audit Officer, Office of the Director General of Audit, Central, Mumbai

1. Background

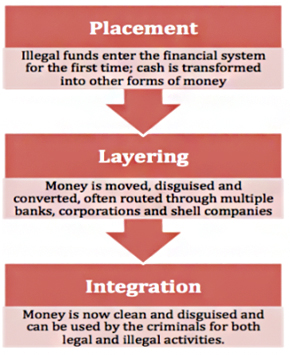

Organization of Economic Cooperation and Development (OECD) in its report on “Misuse of Corporate Vehicles for Illicit Purposes” had flagged the misuse of the separate legal entity/ shell corporations to cloak illicit incomes. The subject has gained increased relevance in the recent period and the Income Tax Department(ITD) has brought out in May 2017 a Status Report on ‘Operation Clean Money’ which presents the strategy and current status of targeting unaccounted money. In report’s Annexure A - Modus operandi operated for unaccounted cash, there is specific section on cash deposits through Shell companies which gives illustration of two cases of conversion of unaccounted cash through Shell companies. This buttresses the fact that Shell companies are being operated on large scale for evading taxes. After the demonetization of high value currency in November 2016, the role played by the so called Shell companies to convert the illicit cash has come into greater focus leading the Government to initiate steps to identify and delegitimize such companies. Given this background it’s imperative for the auditors to also scale up their skills to identify the possible gap areas in the existing tax laws and rules which are exploited by the Shell company operators for evasion of taxes.

2. What is Shell Company?

In simpler terms, just like a shell, which has a thick outer covering, while the inside is hollow, Shell Company is a corporate entity without active business operations or significant assets. It is interesting to note that that shell corporations are not illegal. They are deliberate financial arrangements created to either avoid taxes or even promote startups. Earlier, generally, Shell companies were registered in tax havens, where there is nil or low tax1.

Legally, Securities Act enacted in the USA has defined Shell company as follows.

“Securities Act Rule 405 and Exchange Act Rule 12b-2 define a Shell Company as a company, other than an asset-backed issuer, with no or nominal operations; and either:

- no or nominal assets;

- assets consisting of cash and cash equivalents; or

- assets consisting of any amount of cash and cash equivalents and nominal other assets.”

In India, Shell companies haven’t been defined under the Companies Act, 2013.

2. How does a Shell company operate in India?

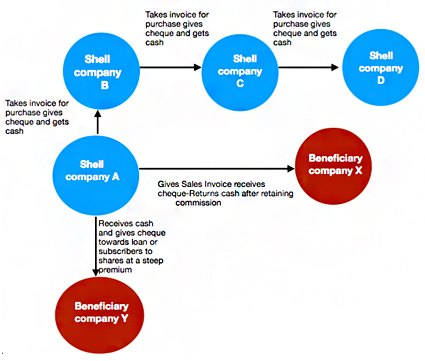

The Shell companies are used in the following manner in India:

- IV. Establishing of Shell companies in tax havens for the purpose of treaty shopping. Siphoning money abroad showing it as investment in foreign subsidiaries and after passage of time writing off the investment due to extinguishment of shares. Shell companies are formed for fictitious exports of software, diamond etc for claiming exemption under Section 10A, 10B etc of Income tax Act, 1961. It also served to bring in amount laundered back to the country without payment of taxes.

- V. Companies float chit fund companies and cash deposited in banks are shown as received from many small investors in cash and the money so received is shown to have invested or lent to several Shell companies and thereafter transferred to the ultimate beneficiaries.

- VI. Companies are also formed for carrying out major works where fictitious purchases and expenses are booked mostly without withholding tax to inflate the capital expenditure. After completion or at times midway before completion of work the Work is transferred to another company to avoid audit trail and any scrutiny of the inflated expenditure.

- VII. Companies are also used to over invoice imports or under invoice exports. Diamond and other traders show purchases at high value from Shell companies to transfer money abroad. Similarly, when money is required to be brought back in India either the import is under invoiced or exports are over invoiced.

- VIII. Companies in generation of electricity are stated to have floated Shell companies for importing coal into India. The coal purchased from Indonesia is invoiced from Dubai or other tax haven at a cost far more than at which is purchase from Indonesia. The companies benefit by getting a higher price because of ‘Fuel adjustment charges’ in their power tariff and also transfer money abroad resulting in dual benefit.

3. Actions by the Government to curb Shell Company Operations

- a) Special Investigative Team(SIT) on Black Money, had flagged the issue of Shell companies in its 3rd Report (July 2015).The recommendations made by SIT in this regard were that Serious Frauds Investigation Office (SFIO) under Ministry of Corporate Affairs(MCA) needs to actively and regularly examine the MCA 21 database for certain red flag indicators and share information on such high risk companies with law enforcement agencies, CBDT and FIU for closer surveillance. SFIO should also refer the matter to Enforcement Directorate for taking action under PMLA for all such cases of money laundering.

In above respect, MCA vide its notification dated 20 September 2017 notified Companies (Restriction on the number of layers) Rules, 2017 restricting the number of layers of subsidiaries for certain classes of holding companies to two layers. The Benami Transactions (Prohibition) Act has been amended to provide for confiscation of Benami properties and Income tax authorities have been mandated to assist in inquiry initiated under this Act. Income Tax Act, 1961 has been amended to impose 60 percent tax and 25 percent surcharge on undisclosed income and investments. The effect of such Amendments is yet to be seen.

- b) Database of Ministry of Corporate Affairs had 15.27 lakh companies registered with it as on January

4. Audit Approach to audit the tax evasion through shell Operations

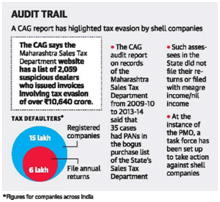

The long para on “Fictitious sales and purchases by Shell Companies/Hawala Operators” which was printed in Chapter V of CAGs Report No. 2 of 2017 (Direct Taxes), highlighted the role played by the entry providers in giving bogus purchase invoices to help reduce the tax liability of the beneficiary companies, firms and concerns. The para was a culmination of sustained efforts made by the Department, particularly as the Income Tax Department was not forthcoming with sharing of information with the Audit.

- In order to audit the complete trail from the entry providers to the beneficiaries, a few of the entry providers mentioned in the list put up by Maharashtra Sales tax department on its website were selected. DGAC, Mumbai identified some 4-5 bogus companies and did complete analysis of their Directors, addresses and thereafter identified all other companies they controlled.

- A nodal Local Audit Party(LAP) was formed to audit the Assessment records of all those companies within their audit jurisdiction. All other LAPs were instructed to look into selected assessees across different charges and database prepared of the sales and purchase shown by them in their books of account. The transactions which indicated layering were eliminated and only those transactions which showed sales to beneficiaries were selected for cross verification. Nodal LAP tried completing trail of transactions wherever possible.

- This database was standardized and 800 cases were cross verified with the records of the entry providers. The results of the verification were compiled in a draft para which was included in CAG’s report. While accepting most of the findings, the Ministry agreed that the present system of assessing such cases needed to be modified.

We noticed that Income Tax Department scrutinizes each case in isolation except in case of search and seizure. Such type of Assessment is not conducive for getting clinching evidence and sustainability of addition in case of Shell companies. As per audit experience, the Income Tax Department only considers the paper trail of invoices received and payments made but does not obtain the bank statements and link it with accounts of the assessees and the beneficiaries. The complete loop of the transactions is seldom verified.

5. Checklist for Auditing Shell Companies

Tackling Shell companies in audit may not be easy as there is no legal definition for Shell Company in the Companies Act 2013. There is no specific law to deal with Shell companies. The current actions are initiated under Benami Transaction (Prohibition) Amendment Act, 2016; Prevention of Money Laundering Act, 2002; Income Tax Act 1961, Companies Act, 2013 by the respective agencies. Besides the companies identified by the different government agencies as Shell companies, tax auditors can also glean through the cases of ex-parte assessment done under Section 144 of the Income Tax Act as many of these assessees are likely to be the companies used for temporary period for conversion of black money and then abandoned.

Ideally a standard check list will have to be prepared to check whether the all requisite documents have been called for by the tax authorities and the results of the examination has been communicated to the assessing charge of the ultimate beneficiaries.

The action taken by the department will have to be captured on a database to check for consistency of approach and whether the data collected from these Shell companies is used to ascertain the ultimate beneficiaries. Big data analytics can be used for the same. A few cases are to be shortlisted for detailed cross scrutiny. The complete loop of these cases is required to be verified right from the Shell companies to the ultimate beneficiaries to pin point any failures.

The checklist should interalia include

- Whether Investigation Wing has carried out proper investigation before designating the company as a Shell company and all the inputs collected during the investigation have been given in a report to the Assessing Officer?

- Whether the Assessing Officer has called for the accounts, details of purchases and sales and correlated it with the payments or receipts and further correlated with the bank accounts? Whether all the inputs collected during the investigation have been given in a report to the Assessing Officer?

- Whether there are significant entries of cash in the bank account or in the account of the company from whom the purchase and sales have been made or in those companies through which the transactions have been layered? Whether the Assessing Officer has called for the accounts, details of purchases and sales and correlated it with the payments or receipts and further correlated with the bank accounts

- Whether all related companies and associates of the companies with common directors or significant transactions were taken up for detailed scrutiny? Whether the information regarding suspicious transactions shared across assessment charges?

- Whether consistent approach is applied to similar situated transactions across companies and under which sections additions are made?

- Whether penalties as per law are levied for proven suspicious transactions or not and follow-up action is taken after raising the demand or just a paper demand is created without any recovery action? Whether consistent approach is applied to similar situated transactions across companies and under which sections additions are made? Whether all sister companies and associates of the companies with common directors or significant transactions were taken up for detailed scrutiny?

- Whether due evidences have been corroborated during assessment to ensure sustainability of additions?

6. Conclusion

A good start in cracking down on domestic Shell companies has been made but we also need to find out and report on the efforts made by the Government in interlinking the information available with different departments to arrive at a logical decision and action taken thereon. In the wake of concerted efforts of Government for digitization of data at various levels, how far the Income Tax Department is able to make use of these data for assessment purpose will have to be seen. The success of the steps taken can only be judged through the final culmination of the cases after they pass through the judicial scrutiny as per the prevailing appellate system, as the real tax benefits shall accrue only once the evidence collected by the tax authorities is found to be sufficient by judicial scrutiny.

- 1. Article by Sandeep Pareek in Financial Express dated 10th August 2017

|