Audit of Project Imports

By Mr. Ravikant Babu, Audit Officer, Office of the Director General of Audit, Central, Mumbai

1. Background

Project imports is a unique concept adopted by India to facilitate faster imports of all machinery/equipment, spares, components and other related materials required for setting up of a new ‘industrial plant’ or for ‘substantial expansion’ of an existing plant. The Scheme seeks to achieve the objective of smooth and quick assessment of imports by providing for a simplified process of classification and valuation. Under this Scheme all goods imported for a project are classified under one chapter heading 9801 of the Customs Tariff Act, 1975 and are subjected to a uniform rate of import duty even though various goods required to be classified in their respective chapter headings as per Harmonised System of Classification and subject to different rates of duty. Project imports also enjoy lower/nil rate of duty than the tariff rate vide notification No.12/2012 Customs dated 17 March 2012 (Previously notification No. 21/2002-cus dated 1 March 2002) issued by Government.

The Scheme is not available to hotels, hospitals, photographic studios, photographic film processing laboratories, photocopying studios, laundries, garages and workshops. It is also not available to a single or composite machine. The below mentioned sectors are eligible for the Scheme.

- Industrial plant

- Irrigation project

- Power project

- Mining project

- Oil/ Mineral exploration project

- Any other projects notified by the Central Government

Scheme allows machinery, prime movers, instruments, apparatus, appliances, control gear, transmission equipment, auxiliary equipment, equipment required for research and development purposes, equipment for testing and quality control, components, raw materials for the manufacture of these items, etc. In addition, spare parts, consumables up to 10% of the CIF (Costs, Insurance and Freight) value of goods.

Statutory Provisions

Scheme is governed by the i) Customs Tariff heading 9801 of the Customs Tariff Act,1975, ii) Project Import Regulations, 1986 (PIR, 86), notified in April 1986 in supersession of PIR 1965; iii) General Exemption Notification No. 12/2012-Customs, dated 17 March 2012 providing for concessional rate/exemption from Basic Customs Duty (BCD) and additional duties of customs i.e. Countervailing Duty (CVD) on goods imported under CTH 98.01, subject to with or without conditions, as specified against each entry; iv) Notification No. 21/2012-Customs, dated 17 March 2012 for exemption from payment of Special Additional Duty (SAD) of customs for certain specified Project Imports, v) Projects notified by Government for benefits under the Scheme by issuing specific notifications, vi) Chapter 5 of CBEC Customs Manual vii) Circulars issued from time to time by the Central Board of Excise and Customs (CBEC) and viii) case laws of judiciary.

Process of registration under Project imports

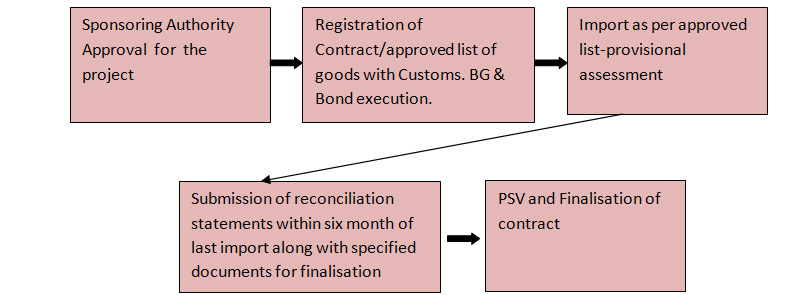

Implementation of the Scheme is governed by regulations 1 to 7 of PIR, 1986. A project must first be approved by a Sponsoring Authority (Ministry/State Government Department and others as notified) to get the benefit of the Scheme. The importer must have entered into a contract with the supplier, got all the goods attested by Sponsoring Authority along with clear specifications of its dimension, quantity, description, CIF values. Such contracts be registered with the Project Import section of Custom port from where the importer intends to import major part of goods. After verifying the requisite documents, the Custom port registers the project contract and allots a registration number. Then only the imports under the Scheme are allowed. The Scheme is available to the main contractor as well as sub-contractor(s) supplying goods to the main contractor. Any changes in contract, specifications shall also be registered with Customs along with Sponsoring Authority’s approval. The importer can also import the goods from ports other than port of registration by availing Telegraphic Release Advice (TRA) facility.

Registration also requires other documents like process flow chart, drawing, design layouts, catalogues, literature of items to be imported, location/s to be installed, detailed engineering agreement, equipment supply agreement, service agreement, or any other agreement with foreign collaborators/suppliers including the details of payment actually made or to be made, industrial licence, import licence, Authority’s certificate whether the goods required for initial set up or for substantial expansion.

All importers, except Government departments and PSUs, have to file Bank Guarantee (BG) @2% of total CIF value upto maximum of one crore, until finalisation of contract, towards protection against any revenue loss. In addition, all importers have to execute a continuity bond equivalent to CIF value.

Importation, assessment and clearance of goods:

Imports are allowed with reference to specifications mentioned in registered contracts; the bill of entry is provisionally assessed under Section 18 of Customs Act 1962 and handed over to the importer for payment of duty. In case of projects, where imports take place over long periods, sometimes extending over a number of years and where action to finalise the cases takes place only after all the imports under the contract have been made, final assessment be completed within six months of the date of import of the last consignment covered by the contract. In normal course, after submission of the reconciliation statement and other documents by the importers, the provisional assessments are finalised within a period of three months where plant site verification is not required and six months where plant site verification is required.

Finalisation of contract

- (a) Submission of reconciliation statement by the importer

The importer shall within three months from the date of clearance for home consumption of the last consignment of the goods or within such extended period as the proper officer may allow, submit (i) a reconciliation statement showing the description, quantity and value of goods imported along with a certificate from a registered chartered Engineer certifying the installation of each of the imported items of machinery, (ii) copies of bill of entry, invoices and final payment certificate (iii) customs copy of the Import Trade Control (ITC) (iv) Exchange control copy of ITC (v) Amendments to the contracts if any and (vi) any other document that may be required by the proper officer for finalisation of the contracts.

- (b) Plant Site Verification (PSV)

The underlying feature of the Scheme is that goods imported must have been used for the project. A PSV is required in cases where value of project exceeds Rs. 1 crore and in other cases at least 10% of the registered project will be subjected to PSV by the jurisdictional Central Excise Office. The PSV shall be completed within fifteen days of submission of relevant documents by the importers. However, in cases of Government Departments and Public Sector Undertakings, the requirement of PSV under project imports can be fulfilled by means of issuing appropriate Certificate by the Head of PSU / Government Undertaking in the rank of Chairman / Executive Director.

Workflow Chart of the Scheme

Considering the significance of Scheme as facilitation measure for setting up of industries and infrastructure projects and procedural requirements of the Scheme, CAG of India undertook a Performance Audit of the Scheme during 2016-17 and the report was presented in the Parliament vide Report No.42 of 2016.

Several shortcomings in the Scheme and procedural delays were highlighted, and revealed how the Scheme has lost out on its primary objective of providing a simplified procedure for quick assessments due to ambiguities in duty structure and procedural hurdles.

Some of the issues are highlighted below:

- Insufficiency in Rules and Procedures: A review of the existing legal provisions of the Scheme reveals considerable ambiguities in the Scheme due to later notifications and amendments. Thus, the assessments are being done in an inconsistent manner leading to under/over valuations and incorrect levy of duty. Lack of appropriate provisions in the regulations to monitor completion of imports; have resulted in many projects lingering for indefinite periods and undue advantage of concessional imports being extended to importers even after the commencement of projects. There are multiple sponsoring authorities for a single project without clear administrative responsibilities as to who is monitoring whether the project has been completed and whether the objective of the project – increase in capacity- has been achieved.

- Weak Compliance to regulatory provisions : Performance audit brought forth numerous instances of weak or incorrect compliance to the existing provisions. Contracts were finalised even in the absence of requisite documents, contracts for substantial expansion of project were allowed without actual verification of the expansion of capacity, and inadmissible imports and undedicated goods were allowed under project imports. Audit noticed several instances of imports of spare parts much in excess of the prescribed ceiling and application of incorrect rates of duty and interest.

- Inadequate trade facilitation: Audit examined aspects of trade facilitation like dwell time1 of cargo, documentation requirements, time taken in finalisation of assessments and contracts and transaction costs2. Audit found instances of delay in clearance of cargo at some of the major ports with delays upto 297 days in some cases. Examination of documentation requirements revealed that multiple documents were required to be submitted by importers and that in several cases importers had not submitted the documents or had submitted the same with delays. Although the time prescribed for finalisation of provisional assessments by the Commissionerates was three months, audit found many cases of delay especially when the imports were effected from ports.

- Monitoring lapses: Even though the Customs Department has computerised its operations through the EDI system, the performance audit revealed that no steps have been taken to integrate the Project Import Scheme within the EDI system.The system does not capture complete data regarding project import transactions. Consequently, it is almost impossible to have a complete overall picture of all the imports being effected under the projects registered under the Scheme, besides making the monitoring of the Scheme highly cumbersome and dependent on manual interventions. Audit found instances of incomplete or non-existent records and reports and missing files pertaining to ongoing contracts which indicated a weak internal control.

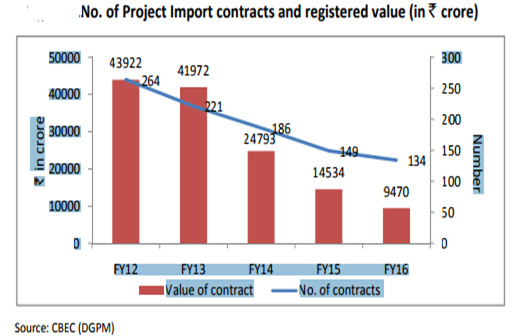

Thus various factors, both systemic and procedural, cause delay in finalisation of contracts in the Scheme. These were not properly addressed by the department so far. As a result the main objectives of the Scheme, simplicity and quick assessments, have been sidelined. The Scheme is mired in cumbersome paperwork, endless delays and has lost sheen to other schemes like Export Promotion Capital Goods(EPCG) Scheme. Now if you take a glance of the statistics of contracts being registered in the last five years it indicates how the Scheme has decelerated.

Current trend of the Scheme:

In the last 5 years(2011 to 2016) the number of contracts registered has declined by 49 per cent from 264 in FY12 to 134 in FY16. The Scheme is losing its advantage to other schemes like EPCG/ Zero duty EPCG for import of capital goods which have been introduced subsequent to Project Imports, under which importers might be availing similar or more benefits. In addition, the fact that overall the custom duty rates have been rationalised and peak duty rates are at an average of 10 per cent, the benefits from project import may not seem very attractive to the importers.

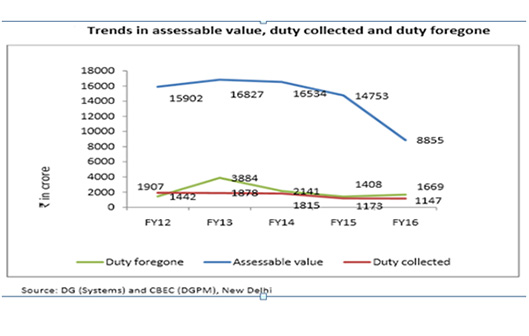

A trend in the assessable values, duty collection and duty foregone also suggest that the Scheme is becoming less attractive among importers.

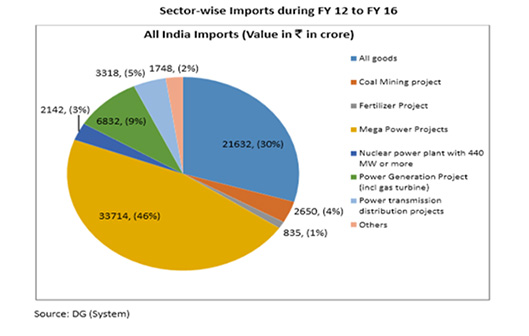

Sector wise analysis of value of imports in last 5 years (2011 to 2016) represents that, power sector projects, had the largest share of project imports among all the sectors eligible for project imports. Within power sector, highest value of imports were in the mega power projects followed by power generation projects, power transmission and distribution projects and nuclear plant projects. Other significant sectors included coal mining projects.

The above analysis indicates that big industrialists having capability of meeting the procedural compliances have utilised the Scheme. Further huge capital outlay projects which enjoy almost nil duties under the Scheme like mega power projects were more successful under the Scheme. Benefit under the Scheme is not uniform across all sectors, though the major advantage of the Scheme has been that it does not put any obligations on importers to achieve any production outcomes or to meet any export targets in lieu of duty concessions extended.

Conclusion:

Decelerating trend in number of contracts registered and revenue generated during past few years when the percentage of new contracts registered under the Scheme has come down by almost half (49 per cent) indicates that importers could be opting for other more beneficial Schemes. In addition, the fact that overall the custom duty rates have been rationalised and peak duty rates are at an average of 10 per cent, the benefits from project import may not seem very advantageous to the importers. Collating data and information on certain trade facilitation measures, it can be seen that the benefits of trade facilitation have not accrued to the Project Imports. In fact, high transaction costs could be keeping away the medium and small scale importers/manufacturers from taking benefits of the Scheme. Further, after introduction of Goods and Services Tax, Integrated Goods and Service Tax(IGST) equivalent to CVD and SAD is payable along with BCD on all imports under the Scheme, resulting in escalation of import cost. This may put the Scheme to further disadvantage compared to other export promotion schemes.

- 1. Dwell time is the measure of the time elapsed between the arrival of goods in the port and their final clearance.

- 2. Transaction cost includes differential cost of credit at international and domestic rates, costs due to procedural delays and costs of transportation delays.

|