CHAPTER 1

GOVERNMENT INVESTMENTS, LOANS & LIABILITIES

1.1 Introductory

(i) The accounts of Government Companies, General Insurance Companies and Deemed Government Companies are test checked and subjected to supplementary audit by the officers of the Comptroller and Auditor General of India (CAG) subsequent to the audit by the Statutory Auditors (Chartered Accountants appointed by CAG). Some of the Statutory Corporations are either audited by CAG as Sole Auditor or by the Chartered Accountants appointed as primary auditors. In the case of latter, the statutes under which the Corporations have been set up invariably provide for supplementary audit by the CAG.

(ii) As on 31 March 2001, 368 Government Companies/Corporations were under the audit jurisdiction of the Comptroller and Auditor General of India. These included 271 Government Companies, 5 Insurance Companies, 6 Statutory Corporations and 86 Deemed Government Companies of the Central Government.

(iii) During the period ended 31 March 2001, fourteen Companies (ten Government Companies and four Deemed Government Companies) came within the purview of the CAG and seven Companies (two Government Companies and five Deemed Government Companies) ceased to be Government Companies. The details are given below:

New Government Companies

- Indian Railway Catering and Tourism Corporation Limited

- Narmada Hydroelectric Development Corporation Limited

- Guru Gobind Singh Refineries Limited

- Chinar Watches Limited

- Rail Tel Corporation of India Limited

- Millennium Telecom Limited

- Instrumentation Digital Controls Limited

- Instrumentation Control Valves Limited

- IL Power Electronics Limited

- Bharat Sanchar Nigam Limited

New Deemed Government Companies

- Ahmedabad Vadodara Expressway Company Limited

- Millennium Information System Limited

- Gujarat Chemical Port Terminal Company Limited

- IDBI Trusteeship Services Limited

Ceased Government Companies

- Bharat Aluminium Company Limited

- Lagan Jute Machinery Company Limited

Ceased Deemed Government Companies

- Kanhangad Rubbers (P) Limited

- Kanjirapalli Rubbers (P) Limited

- Kozhikode Rubbers (P) Limited

- Manimalayar Rubbers (P) Limited

- Pazhassi Rubbers (P) Limited

Of the six Statutory Corporations whose accounts were required to be audited by CAG under the respective Statutes, four Corporations, namely, Airports Authority of India, Damodar Valley Corporation, Inland Waterways Authority of India and National Highways Authority of India were solely audited by CAG. In respect of Food Corporation of India, the audit of which was being conducted in addition to the audit by Chartered Accountants, CAG was made sole auditor of the Corporation by an amendment to the Food Corporation Act, 1964 in June 2000. In respect of another Corporation i.e. Central Warehousing Corporation, CAG has the right to carry out supplementary audit in addition to the audit carried out by the Chartered Accountants as primary auditors.

(v) Ministry and Department wise details of Public Sector Undertakings [PSUs] are given in Appendix I. Ministry/Department-wise details indicating the types and numbers of Government Companies, General Insurance Companies, Statutory Corporations which were subject to audit by the Comptroller and Auditor General of India as of 31 March 2001 are given in Appendix II A and II B. The equity investment in and loans given to these companies by the Central Government, Central Government Companies/Corporations, State Governments and others are also indicated therein. These Appendices do not, however, show the details of 10 PSUs which are defunct/under liquidation, 10 PSUs which have not submitted their accounts for any of the years since their incorporation/becoming a deemed Government company and 15 PSUs which have not submitted their accounts for the last 3 years or more.

(vi) Under Sections 166, 210, 230, 619 and 619-B of the Companies Act, 1956, read with Section 19 of the Comptroller and Auditor General’s (DPC) Act, 1971, the accounts of the Companies for the financial year are to be submitted for audit within 6 months from the end of the relevant financial year. More or less similar provisions exist in the statutes governing various statutory corporations. Audited accounts of Government Companies/ Corporations are required to be laid on the table of both the Houses of Parliament within a Period of 9 months from the end of the financial year. The accounts of 285 companies (including 58 Deemed Government Companies) for the current year were submitted for audit by the stipulated date i.e. 30 September 2001. In respect of 54 (Includes 6 companies fro which audit was in progress) PSUs (including 10 Deemed Government Companies), provisional figures have been adopted in this report based on the latest audited accounts. The details of 48 PSUs as well as 35 PSUs/deemed Government Companies (identified in the appendix by two asterisks - **) referred to in sub-para (v) above, are indicated in Appendix - III.

1.2 Budgetary Outgo

(i) Outgo from the Union Budget to the PSUs during the last three years showed an increasing trend. The outgo for the year 2000-01 was Rs.3942.81 crore more as compared to 1999-2000. This represents an increase of 21.12 per cent as indicated in the Chart 1 below:

(ii) The table below indicates the structural composition of budgetary contribution towards equity capital, loans and subsidy related to administered prices of PSUs:

Budgetary Outgo

(Rs. in crore)

|

1998-99 |

1999-00 |

2000-01 |

|

|

Total Outgo* |

16406.49 |

18664.66 |

22607.47 |

|

Outgo on account of subscription to Equity Capital |

3984.25 |

4343.35 |

2358.94 |

|

Outgo due to Loans given |

1422.76 |

2665.98 |

3854.72 |

|

Subsidy related to administered prices |

10999.48 |

11655.33 |

16393.81 |

* Provisional figures of subsidy (Rs.8646 crore, Rs. 8856 crore, and Rs. 11462 crore for the years 1998-99, 1999-00 and 2000-01 respectively) received by Food Corporation of India has been included as intimated by the management because the accounts for the last three years of the Corporation are in arrears.)

(iii) The proportion of outgo through subsidy relating to administered prices as paid/payable to PSUs has increased by 5394.33 crore (49.04 per cent) as compared to 1998-99 and by Rs.4738.48 crore (40.65 per cent) when compared to outgo in the previous year. Out of total subsidy outgo for the year 2000-01, Rs.11462 crore (69.92 per cent) was given to Food Corporation of India. (See table above and graphs below). The outgo by way of Loans increased by Rs.1188.74 crore (44.59 percent) over the previous year, especially in sectors like Coal, Mines and Power. Government continued to subscribe to equity in PSUs and made a further investment of Rs.2359 crore.

1.3 Waiver of Dues

Indirect assistance by way of moratorium on repayment of loans or write off and waiver of interest has been a constant feature of Governments’ supportive role to PSUs. The table below indicates the details of such assistance for the last three years ending March 2001. The indirect assistance to PSUs during the current year had, however, decreased by Rs.4246 crore (68.45 per cent) when compared to 1999-2000. Out of the total waiver of dues, Rs.1482 crore (75 percent) were in the steel and surface transport sectors.

WAIVER OF DUES

(Rs. in Crore)

|

1998-99 |

1999-00 |

2000-01 |

|

|

1. Loan repayments written off |

392.26 |

5073.00 |

226.15 |

|

2. Interest waived |

1168.13 |

984.20 |

1466.36 |

|

3. Penal interest waived |

209.02 |

134.09 |

138.11 |

|

4. Repayment of Loan on which moratorium allowed |

376.93 |

12.14 |

126.79 |

|

Total |

2146.34 |

6203.43 |

1957.41 |

1.4 Guarantees given by Central Government

Besides budgetary outgo and waiver of dues, Central Government extends support to PSUs by way of guarantees for loans availed by the PSUs at a nominal fee. The total amount guaranteed during 2000-01 increased substantially by 140.39 percent as compared to the previous year and when compared to1998-99 increased by 260.96 percent.

Guarantees Given by Central Government

(Rs. in crore)

|

Guarantees |

Amount Guaranteed During |

Guaranteed Amount outstanding as on 31 March 2001 |

||

|

1998-99 |

1999-00 |

2000-01 |

||

|

1. Cash Credit from State Bank of India (SBI) and other Nationalised Banks |

1832.93 |

1624.94 |

1654.33 |

1268.69 |

|

2. Loans from other Sources |

806.17 |

944.91 |

8519.80 |

1968.67 |

|

3. Letters of Credit opened by SBI in respect of Imports |

979.87 |

1495.86 |

2329.08 |

604.31 |

|

4. Payment Obligations under agreements with Foreign Consultants or Contractors |

439.82 |

2028.67 |

2147.33 |

1311.93 |

|

Total |

4058.79 |

6094.38 |

14650.54 |

5153.60 |

1.5 Investment in Central Government Companies and Corporations

(i) Audit received accounts of 227 PSUs out of 282 Central Government Companies and Corporations in existence at the end of 2000-01. The data for three new Government Companies has been included in the current year’s figure. The equity investment of the Government of India in 263 (Excludes 2 companies (HMT Chinar Watches Limited and HMT Tractors limited) for which data was not complete) companies/corporations (whose accounts have been reflected in the report) and Food Corporation of India (whose accounts are in arrears for the last three years ending 2000-01) and loans given to them amounted to Rs.79,080.53 crore and Rs.43,259.50 crore respectively. Some Central Government Companies/ Corporations have also contributed to the investment in these public sector undertakings. The details are given below:

(Rupees in Crore)

|

As on 31 March 2001 |

As on 31 March 2000 |

|||||

|

Sources |

Equity |

Loans |

Total |

Equity |

Loans |

Total |

|

1.Central Government * |

79080.53 |

43259.50 |

122340.03 |

73340.55 |

39082.65 |

112423.20 |

|

2.Central Government Companies/ Corporations |

11093.24 |

9963.92 |

210571.16 |

10563.90 |

11149.07 |

21712.97 |

|

3.State Governments/ State Government Companies/ Corporations |

2025.21 |

491.72 |

2516.93 |

1754.88 |

429.29 |

2184.17 |

|

4. Others |

3218.29 |

123480.67 |

126698.96 |

2744.94 |

116083.17 |

118828.11 |

|

Total |

95417.27 |

177195.81 |

272613.08 |

88404.27 |

166744.18 |

255148.15 |

|

Percentage of Central Government Investment |

82.88 |

24.41 |

44.88 |

82.96 |

23.44 |

44.06 |

* Includes Rs.2252.10 crore towards equity in Food Corporation of India.

(ii) During 2000-01, the investment in equity and loans to these PSUs had registered a net increase of Rs.7013 crore and Rs.10,451.63 crore respectively. [See Chart 4 (a) and 4(b)]. Government of India has significantly enhanced its investment in the equity of PSUs under the Ministries of Surface Transport (Rs.2,207.35 crore), Power (Rs.973.34 crore), Atomic Energy (Rs.586.00 crore), Heavy Industry (Rs.1,248.46 crore), Urban Affairs and Poverty Alleviation (Rs.280.00 crore) and Railways (Rs.192.98 crore). PSUs under the Ministry of Fertilizers (Rs.4257.99 crore), Textiles (Rs.495.29 crore), Power (Rs.440.19 crore), Railways (Rs.402.76 crore), Heavy Industry & Public Enterprises (Rs.333.91 crore), Mines (Rs.325.52 crore) and Atomic Energy (Rs.244.74 crore) also received additional Government Loans.

1.6 Central Deemed Government Companies

(i) Section 619-B of the Companies Act, 1956 lays down the criteria for determining whether a company is a Deemed Government Company i.e., whether 51 percent or more of its paid up share capital is held by Central / State Governments, Central/State Government Companies and Corporations owned or controlled by the Government. According to information available, there were 86 Deemed Central Government Companies as on 31 March 2001 as listed in Appendix - IV.

(ii) The capital invested by the Central Government and by Companies and Corporations controlled by it in 68 Deemed Government Companies (whose accounts were reviewed during the year) is given in Appendix V (see also Chart 5). Out of the remaining 18 Deemed Government Companies, 9 were either under liquidation or were defunct. The accounts of 6 Companies were not reviewed as the accounts of these companies were in arrears for more than 3 years, while the accounts of other 3 companies were not made available to audit right from the dates of their inclusion under audit purview.

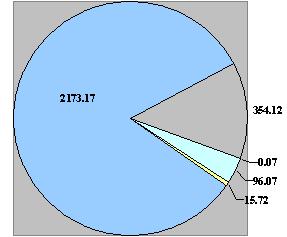

(iii) As of 31 March 2001, equity of Rs. 2,639.15 crore in 68 Deemed Government Companies was contributed by the Government of India (Rs 0.07 crore in 2 companies), State Governments (Rs.2.26 crore in 4 companies), Central Government Companies / Corporations (Rs.96.07 crore in 14 companies), State Government Companies / Corporations (Rs.13.46 crore in 14 companies), Financial Institutions / Banks (Rs.2,173.17 crore in 36 companies) and others (Rs.354.12 crore in 26 companies).

| Chart-5

Composition of Shared Capital in Deemed Goverment Companies |

|

|

|

(iv) Out of 68 Deemed Government Companies reviewed in this Report, 41 Companies earned profit. Of these only 22 declared dividend amounting to Rs.144.02 crore which represented 11.49 per cent of their total paid up capital. 27 Companies including one company in which Government of India had invested incurred loss during 2000-01.

(v) Dividend of Rs.144.02 crore declared by the Deemed Government Companies during 2000-01 was mainly from the companies under Financial and Trading Sectors as indicated below:

(Rs. in crore)

|

Sector |

No. of Companies |

Paid up Capital |

Net Profit |

Dividend |

|

1. Financial Sector |

15 |

652.73 |

357.81 |

81.88 |

|

2. Trading Sector |

2 |

600.00 |

161.10 |

62.01 |

|

3.Consultancy Sector |

5 |

0.95 |

1.37 |

0.13 |

|

Total |

22 |

1253.68 |

520.28 |

144.02 |

1.7 Disinvestment Policy of the Government

(i) Disinvestment Commission was set up on 23 August 1996 for a period of 3 years to draw a comprehensive overall long term Disinvestment programme, to determine the extent of Disinvestment, to monitor the progress of Disinvestment process and to take necessary measures and report periodically to Government on such progress etc. The terms of reference were modified on 12 January 1998 to include that it will be an advisory body and its role and function would be to advise the Government on disinvestment in those Public Sector Units that were referred to it by the Government.

(ii) For decision making and implementation, there is a three tier mechanism in Government viz., Cabinet Committee on Disinvestment (CCD), Core Group of Secretaries on Disinvestment (CGD) and Inter-Ministerial Group (IMG).

(iii) The salient features of the policy of disinvestment of shares of the PSUs are:

- Restructuring and reviving potentially viable PSUs;

- Closing down PSUs which cannot be revived;

- Bringing down Government equity in all non-strategic PSUs to 26 percent or lower, if necessary; and

- Fully protect the interest of the workers;

(iv) 72 Public Sector Units were referred to Disinvestment Commission out of which 47 were making profit. In its report on 58 PSUs, the Disinvestment Commission recommended deferment of disinvestment in respect of 11 PSUs and non disinvestment of one PSU. For the remaining 46 PSUs, Disinvestment Commission suggested following methods of sale:

|

Method of Sale |

No of PSUs |

|

Strategic Sale |

29 |

|

Trade Sale |

8 |

|

Offer of Sale |

5 |

|

Closure / Sale of Assets |

4 |

|

Total |

46 |

(v) Though the Government of India had since realized Rs.20,261 crore from 1991-92 to 2000-01 from disinvestment of its shares in 42 PSUs, it had privatised only five companies during the years 1999-2001 through strategic sale. These are:

- Lubrizol India Limited

- Indian Additives Limited

- Modern Food Industries (India) Limited

- Bharat Aluminium Company Limited

- Lagan Jute Machinery Company Limited

(vi) During the year 2000-01, disinvestment of Government shares was made in Kochi Refineries Limited and Government had realized Rs.659.10 crore by disposing 758.897 lakh shares of Rs.10 each from Bharat Petroleum Corporation Limited. Similarly, in respect of Chennai Petroleum Corporation Limited, Government had realized Rs.509.33 crore from Indian Oil Corporation Limited by disposing 772.652 lakh shares of Rs.10 each. Government had also realised Rs.148.79 crore from Indian Oil Corporation Limited by disposing of 1487.94 lakh shares of Rs.10 each of Bongaigaon Refineries and Petrochemicals Limited.

(vii) Disinvestment of shares of these three companies was not disinvestment in its true spirit as contemplated in the Disinvestment policy of the Government but a mechanism developed by the Government to generate the revenue to meet the budgetary deficit of Central Government.